For the first time in DeFi, tokenized securities can serve as productive collateral in lending markets without giving up the permissioned transfer framework they require.

Euler has launched a new type of ERC-4626 vault for permissioned assets, made possible by our modular infrastructure.

Developed in close collaboration with Securitize, the vault is designed for regulated real-world assets that need to preserve distinct transfer, ownership, and eligibility requirements while participating in DeFi lending markets.

The vault brings assets like tokenized funds into lending markets by enforcing transfer checks at the contract level. Asset-specific restrictions live around the collateral, while the core lending infrastructure remains modular and permissionless.

That opens the door for a wider class of institutional collateral to enter transparent, programmable lending markets.

Many real-world assets cannot move like ordinary ERC-20s. Tokenized funds, credit products, and other regulated assets may carry eligibility requirements, issuer controls, beneficial ownership records, freeze obligations, re-registration processes, or approved liquidation paths.

These are not incidental details. They are part of how the asset is issued, held, and transferred. Any lending market that uses these assets as collateral has to preserve those requirements onchain rather than routing around them.

DeFi’s strongest properties come from a clean premise: markets should be open, transparent, permissionless, and governed by code.

Public contracts. Self-custody. Open verification. Composable infrastructure. Markets that do not depend on private gatekeepers to function.

But that premise can turn into a false binary: open or closed, permissionless or permissioned, decentralized or institutional.

Assets do not need to become fully permissionless to be useful onchain.

Euler is built to meet assets where they are: preserving the rules that define how they can move, bringing that functionality into DeFi lending markets, and doing it without disrupting the audited core protocol underneath.

The first live example is KPK’s Securitize markets on Euler.

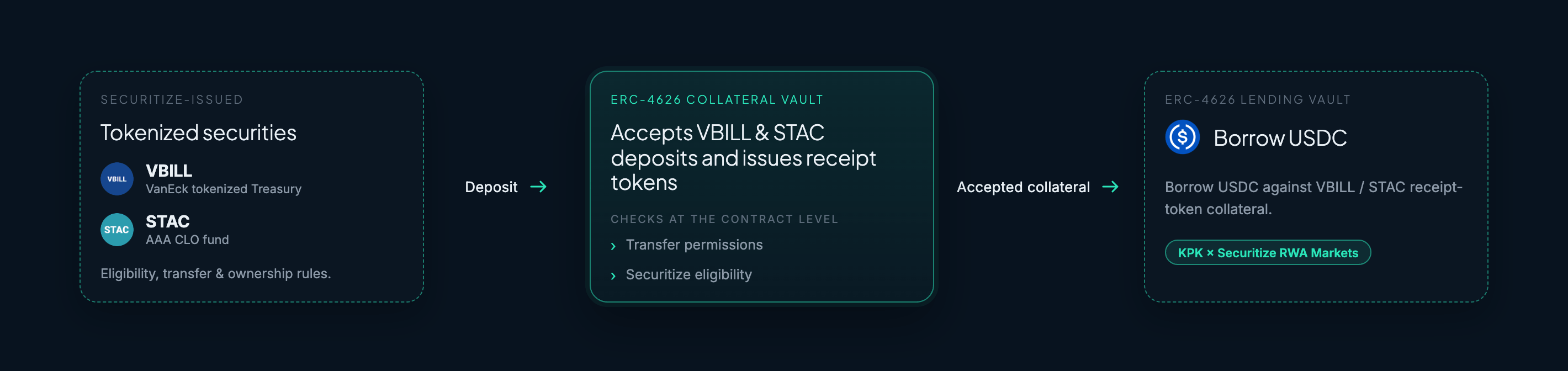

These markets bring Securitize-issued assets such as VBILL, VanEck’s tokenized Treasury fund, into Euler lending markets while enforcing eligibility and transfer permissions at the contract level.

STAC, a tokenized AAA CLO fund, follows the same structure.

For issuers and market creators, this expands the range of collateral that can be supported in DeFi lending.

Each asset sits inside a collateral-only ERC-4626 vault. A holder deposits VBILL or STAC, receives receipt tokens, and can use those tokens as collateral through the EVC.

Borrowing happens separately in a USDC Euler borrow vault configured for that market.

The vault preserves the asset’s transfer rules at each point where collateral can enter or move through the market.

‘deposit and mint’

When a holder deposits a Securitize asset, the vault mints ERC-4626 receipt tokens that Euler can recognize through the Ethereum Vault Connector (EVC).

The vault first checks that the caller and receiver share common EVC ownership. That means a user can deposit into their own account structure, including their EVC sub-accounts, but cannot deposit a permissioned asset and mint collateral into an unrelated owner’s account.

This keeps the position tied to the same account family as the eligible holder. The asset becomes usable as collateral in Euler without breaking the ownership boundary around the underlying Securitize token.

‘transfer and transferFrom’

When ‘transfer’ or ‘transferFrom' is called, the vault checks whether the movement stays within the same EVC owner family or crosses to a different owner. Same-owner movement can follow normal account logic, which lets users manage collateral across their own EVC account structure.

Cross-owner movement is restricted. It is only allowed through controlled paths, such as liquidation or controller-authorized collateral handling, and the recipient still has to pass the Securitize transfer check for the underlying asset exposure.

That gives the market the collateral movement it needs to function, while preventing the position from becoming freely transferable.

Liquidation

In a standard DeFi market, a liquidator can repay debt and receive collateral if the account becomes unhealthy. With permissioned assets, the collateral cannot be transferred freely. The recipient has to be eligible to hold or process the underlying asset.

KPK and Securitize therefore coordinate liquidation through an approved third-party liquidator. That party is whitelisted for the relevant Securitize asset, so it can receive the collateral position if liquidation is required.

Before Securitize collateral can move across owners, the vault checks that the transfer is happening through `preTransferCheck` and runs Securitize’s recipient eligibility check against the underlying asset amount.

If the recipient is not approved, the collateral transfer fails.

That keeps liquidation available as a market safeguard without turning the asset into freely transferable collateral. The borrower’s position can be unwound through Euler’s liquidation system, but only through a recipient that Securitize has approved to handle the asset.

This model gives DeFi more room to grow.

Euler V2 is modular lending infrastructure. New collateral types and market structures can be supported through market-specific vault designs and collateral logic, while the underlying lending engine remains unchanged.

A tokenized Treasury fund should not be forced into the same design as ETH collateral. A permissioned credit product should not need a bespoke lending protocol just to preserve its transfer framework.

Euler is built for this design space.

Bring the asset. Set the rules. Launch the market.

The result is a lending design that can adapt to the asset.

Permissioned assets keep their transfer and eligibility requirements. Market creators can configure collateral support around those requirements without rebuilding the lending stack. Euler’s core infrastructure stays permissionless and transparent, while asset-specific rules are enforced at the vault level.

The next phase of onchain finance will not be one uniform market for every asset.

It will be many markets, with different rules, built on modular infrastructure.

The Securitize-compatible ERC-4626 wrapper has been reviewed by Pashov Group and yAudit.

This article is informational only and is not financial, legal, tax, or investment advice. Euler provides lending and collateral infrastructure. Euler does not manage, sponsor, advise, or distribute the underlying assets or funds. Eligibility to access or transfer tokenized assets may be restricted, and DeFi markets involve risks including smart contract, oracle, liquidation, liquidity, collateral asset, stablecoin, regulatory, and total loss risk.

This content is brought to you by Euler Labs, which wants you to know a few important things.

This piece is provided by Euler Labs Ltd. for informational purposes only and should not be interpreted as investment, tax, legal, insurance, or business advice. Euler Labs Ltd. and The Euler Foundation are independent entities.

Neither Euler Labs Ltd., The Euler Foundation, nor any of their owners, members, directors, officers, employees, agents, independent contractors, or affiliates are registered as an investment advisor, broker-dealer, futures commission merchant, or commodity trading advisor or are members of any self-regulatory organization.

The information provided herein is not intended to be, and should not be construed in any manner whatsoever, as personalized advice or advice tailored to the needs of any specific person. Nothing on the Website should be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any asset or transaction.

This post reflects the current opinions of the authors and is not made on behalf of Euler Labs, The Euler Foundation, or their affiliates and does not necessarily reflect the opinions of Euler Labs, The Euler Foundation, their affiliates, or individuals associated with Euler Labs or The Euler Foundation.

Euler Labs Ltd. and The Euler Foundation do not represent or speak for or on behalf of the users of Euler Finance. The commentary and opinions provided by Euler Labs Ltd. or The Euler Foundation are for general informational purposes only, are provided "AS IS," and without any warranty of any kind. To the best of our knowledge and belief, all information contained herein is accurate and reliable and has been obtained from public sources believed to be accurate and reliable at the time of publication.

The information provided is presented only as of the date published or indicated and may be superseded by subsequent events or for other reasons. As events and markets change continuously, previously published information and data may not be current and should not be relied upon.

The opinions reflected herein are subject to change without being updated.