Liquidity begets more liquidity

“The problem with Uniswap and Euler trying to be all, like, modular, is that liquidity will fragment if there’s loads of pools for each type of asset.”

Here’s why this is a flawed perspective.

Left to its own devices, liquidity typically begets more liquidity. Whenever there are redundant options for where liquidity can flow to, the least liquid options often suffer.

This phenomenon plays out in nature just as much as it does in economics. It’s why you seldom see two species occupying identical niches in the same place at the same time.

The evolutionary process is called ‘positive frequency dependent selection’, and occurs when ‘the more common a variant is in a population, the higher its fitness is.’

In business and economics, this concept forms the foundation of what is often referred to as ‘a moat.’

New social media and dating apps often find it hard to compete with existing ones, even if they offer a better product, because established, albeit worse, apps have more users, and users are a key part of what makes a social media or dating app product great.

The same is true for DeFi protocols.

Liquidity niches

So, if liquidity begets liquidity, why do newer DeFi protocols like Uniswap and Euler plan to allow creators to deploy multiple kinds of pools for each underlying asset market?

It’s because different kinds of liquidity pools are expected to flourish in different niches.

Suppose a lending protocol lets people earn interest on two different USDC markets.

One is exposed to just a handful of blue chip collaterals and pays a moderate amount of interest. The other is exposed to a larger list of long tail assets, paying a higher rate of interest.

The USDC liquidity flowing into these two markets is fragmented because its beneficiaries have different wants and needs.

There is no way to condense this liquidity without breaking the utility the two underlying markets provide. The fundamental issue is that you can’t earn a higher yield without taking on more risk.

The two markets exist and thrive because they operate in different niches, just like different species specialise and thrive in their own different niches in nature. They might share similar properties, but they are not the same market.

This kind of liquidity fragmentation is the sign of a healthy economy. It is not problematic. It would be naive to think that offering users less choice or a single best-of-both-worlds option would make for a better, more capital efficient, protocol.

It might work for a short while, but free markets always find a way to provide users with what they want.

Good vs bad liquidity fragmentation

Liquidity fragmentation is bad when it results from artificial constraints in protocol design.

For example, a lending protocol that only allows pairs of assets to be listed together artificially forces capital to be used in a capital inefficient way.

As a USDC lender I might be happy to lend to borrowers who put up BTC, ETH, and LINK as collateral. But if there are only USDC/BTC, USDC/ETH, USDC/LINK lending pairs, then I have to choose upfront which market to lend to, and probably need to rebalance between them over time.

Lender needs to choose upfront which market to lend (and probably rebalance overtime)

Note that this isn’t a capital inefficient setup for the lenders that legitimately want to isolate collateral risk, but it is capital inefficient for users who are happy to take on more risk.

It is also especially capital inefficient for borrowers. Rather than borrowing from a single larger USDC pool with a more stable interest rate, they need to seek out a less liquid isolated pair.

Euler is a meta lending protocol

What sets Euler v2 apart from other lending protocols is that it empowers creators to build any type of lending protocol they desire, in a permissionless manner.

In that sense, Euler is a meta-lending protocol; an infrastructure layer for global credit markets, not a particular lending product.

Builders can completely recreate something like Aave v3, Compound v3, Morpho Blue, Silo, and more. And then they can connect them to one another!

Liquidity fragmentation will not be a problem because:

a) There are no artificial constraints in Euler v2 forcing users to build only pairs or clusters. They can build anything they wish.

b) Liquidity will flow to markets that occupy a niche. Within that niche, liquidity will attract more liquidity, a winner will emerge, and redundant markets will fade away.

How to build a moat on Euler

You can build vaults on Euler and design them however you like. You will earn 50% of the fees on your vault. So what should you build?

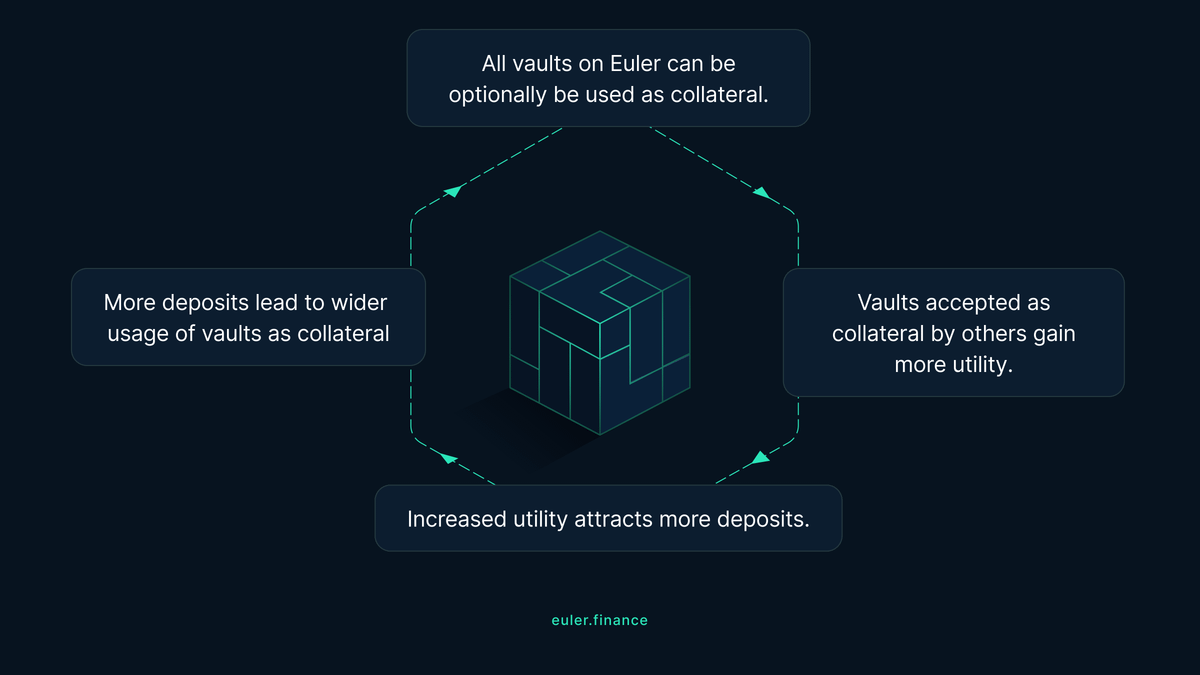

Crucially, all markets on Euler can be optionally used as collateral for all other markets on Euler. No other lending protocol today offers this level of flexibility. This means you should build vaults likely to be accepted as collateral by other vaults. Why?

Because if your vault is accepted as collateral by another vault, it has more utility. If it has more utility, it will get more deposits. And if it gets more deposits, it will likely be used as collateral for yet more vaults.

Positive frequency dependent selection.

If you're interested in building on Euler, check out the docs here and jump into the community discord to get advice on where to get started.

This content is brought to you by Euler Labs, which wants you to know a few important things.

This piece is provided by Euler Labs Ltd. for informational purposes only and should not be interpreted as investment, tax, legal, insurance, or business advice. Euler Labs Ltd. and The Euler Foundation are independent entities.

Neither Euler Labs Ltd., The Euler Foundation, nor any of their owners, members, directors, officers, employees, agents, independent contractors, or affiliates are registered as an investment advisor, broker-dealer, futures commission merchant, or commodity trading advisor or are members of any self-regulatory organization.

The information provided herein is not intended to be, and should not be construed in any manner whatsoever, as personalized advice or advice tailored to the needs of any specific person. Nothing on the Website should be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any asset or transaction.

This post reflects the current opinions of the authors and is not made on behalf of Euler Labs, The Euler Foundation, or their affiliates and does not necessarily reflect the opinions of Euler Labs, The Euler Foundation, their affiliates, or individuals associated with Euler Labs or The Euler Foundation.

Euler Labs Ltd. and The Euler Foundation do not represent or speak for or on behalf of the users of Euler Finance. The commentary and opinions provided by Euler Labs Ltd. or The Euler Foundation are for general informational purposes only, are provided "AS IS," and without any warranty of any kind. To the best of our knowledge and belief, all information contained herein is accurate and reliable and has been obtained from public sources believed to be accurate and reliable at the time of publication.

The information provided is presented only as of the date published or indicated and may be superseded by subsequent events or for other reasons. As events and markets change continuously, previously published information and data may not be current and should not be relied upon.

The opinions reflected herein are subject to change without being updated.